Centrelink deeming rates are the assumed rates of return the Australian Government uses to calculate how much income you are deemed to earn from your financial assets when working out your eligibility for payments like the Age Pension. Instead of looking at every dollar of interest and investment income you actually receive, Services Australia applies standard deeming rules and adds this deemed income to your other income under the means test.

In this guide, you’ll learn what Centrelink deeming rates are, which assets and payments they apply to, how the calculations work in practice, recent changes to the rates, and practical strategies to manage their impact on your retirement income. You’ll also find links to authoritative external resources so you can check the latest rates and run your own estimates.

You can always check the current official deeming settings on the Services Australia deeming page.

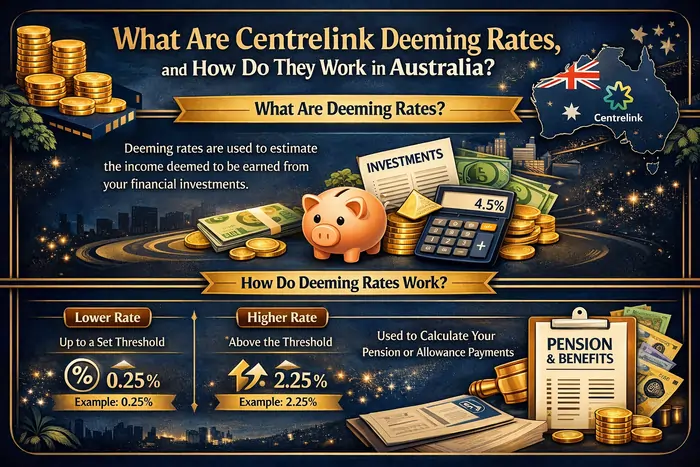

What Are Centrelink Deeming Rates?

Centrelink deeming rates are fixed percentages the government uses to estimate the income you earn from financial assets such as bank accounts, term deposits, shares and managed funds. The system assumes your investments earn a certain return, even if your actual return is higher or lower, and this assumed return becomes your “deemed income” for social security purposes.

Under the deeming rules, Services Australia does not track every interest credit or dividend you receive; instead, it multiplies the total value of your financial assets by the relevant deeming rates and uses that figure in the income test. This simplifies administration and is designed to treat people with the same level of financial assets in a similar way, regardless of how those assets are invested.

You can read a formal definition and policy explanation in the Social Security Guide – Overview of deeming, published by the Department of Social Services (DSS).

Why the Government Uses Deeming

The deeming system exists to make income assessment from investments more predictable, consistent and harder to game. If Centrelink relied solely on actual investment income, people could move money into low‑yield accounts just before an assessment date to artificially reduce their payments under the income test.

According to DSS, deeming encourages people to choose investments based on their merits rather than on how they affect their pension, because returns above the deeming rate are ignored for income‑test purposes. At the same time, using standard deeming rates minimises fluctuations in payment amounts, since small market movements do not constantly feed through to income calculations.

For more background on how deeming fits into social security policy, see the DSS social security deeming rates page.

Which Payments and Benefits Use Deeming Rates?

Deeming rates are used across a wide range of social security and veterans’ payments where a means test includes income from financial assets. Key payments include:

- Age Pension

- Disability Support Pension

- Carer Payment

- JobSeeker Payment and some other working‑age income support payments

- Parenting Payment and some allowance payments in specific circumstances

- Certain Department of Veterans’ Affairs (DVA) income‑support style payments, where Centrelink means tests are mirrored.

The same deeming rules and rates are also used when assessing eligibility for the Commonwealth Seniors Health Card (CSHC), even if you do not receive an income support pension. Independent guidance from SuperGuide explains how deeming rates and thresholds apply to CSHC and Age Pension assessments

You can see how deeming interacts with the Age Pension income test on the Services Australia income test for Age Pension page.

Which Assets Are Subject to Deeming?

Deeming applies to a defined list of financial assets rather than all of your property and possessions. According to DSS and Services Australia, financial assets typically include:

- Cash in bank, credit union and building society accounts

- Term deposits and other fixed‑interest investments

- Shares in listed companies and other equity investments

- Units in managed funds and exchange‑traded funds (ETFs)

- Certain debentures, bonds and similar securities

- Account‑based income streams (allocated pensions) that are assessable under the deeming rules

- Some superannuation interests, particularly once you reach Age Pension age and your super is in the retirement phase.

By contrast, several asset types are either exempt from deeming or treated under specific rules. For example, your principal home is not a financial asset for deeming purposes, and some annuities or structured products may be assessed differently depending on when they were purchased and how they are structured under social security law.

For a detailed breakdown of which investments are deemed and how, see:

How Deeming Rates Work in Practice

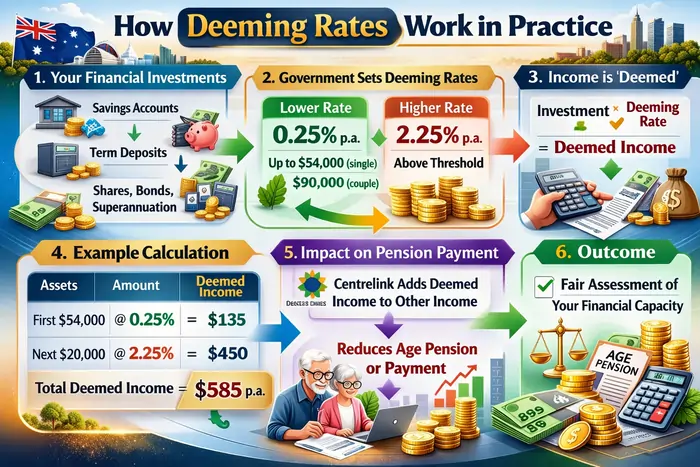

Deeming rates work on a tiered basis: a lower rate applies up to a certain financial‑asset threshold, and a higher rate applies to amounts above that threshold. The current structure differentiates between singles and couples, and in some cases between couples where at least one person receives a pension and couples where neither does.

For the 2025–26 year, Australian Retirement Trust summarises the Age Pension deeming rates as:

- For singles:

- 0.75% on the first 64,200 AUD of financial assets

- 2.75% on financial assets above 64,200 AUD

- For couples (at least one on a pension):

- 0.75% on the first 106,200 AUD of combined financial assets

- 2.75% on combined financial assets above 106,200 AUD

These figures reflect policy changes announced by the Minister for Social Services and explained in the government’s impact analysis on resetting social security deeming rates.

Official guidance from DSS confirms that Services Australia calculates deemed income by multiplying the value of financial assets by these rates and then adding the result to any other income to apply the means test. The current official rate schedule is available on the DSS social security deeming rates page.

Step‑by‑Step Example: Single Person

To see how deeming rates work in the real world, consider a single Age Pensioner with the following financial assets:

- 30,000 AUD in a bank savings account

- 25,000 AUD in term deposits

- 20,000 AUD in shares

Their total financial assets are 75,000 AUD. Under the current deeming structure for singles:

- The first 64,200 AUD is deemed to earn 0.75% per year.

- The amount above 64,200 AUD (in this case, 10,800 AUD) is deemed to earn 2.75% per year.

The annual deemed income is calculated by applying the lower rate to the first tier, and the higher rate to the remainder. Once that annual figure is found, Centrelink converts it to a fortnightly amount and adds it to any other assessable income under the Age Pension income test.

A practical way to model your own situation is to use the SuperGuide Age Pension deeming calculator, which explains the calculation and lets you enter your asset values.

Step‑by‑Step Example: Couple

Now consider a couple where at least one partner receives the Age Pension and they have:

- 40,000 AUD in joint bank accounts

- 60,000 AUD in term deposits

- 30,000 AUD in managed funds

Their combined financial assets are 130,000 AUD. Under the couple deeming rules:

- The first 106,200 AUD of combined financial assets is deemed at 0.75%.

- The remaining 23,800 AUD is deemed at 2.75%.

The resulting deemed income is then used in the couple income test to determine their combined Age Pension entitlement. The same thresholds and rates are used whether the assets are held jointly or individually, as long as they belong to the couple and are financial assets under the deeming rules.

Again, you can test different asset combinations using the SuperGuide Age Pension deeming calculator.

How Deeming Affects Your Centrelink Payments

Deemed income from your financial assets feeds directly into the income test applied to your Centrelink payment. For the Age Pension, the income test looks at your assessable income (including deemed income plus other earnings) and compares it to income‑free areas and cut‑off limits.

If your deemed income and other assessable income stay below the income‑free threshold, your payment is not reduced due to the income test. Once your income goes above that level, your pension gradually reduces at a taper rate until it eventually cuts out entirely at the upper income threshold.

Services Australia sets and updates these thresholds regularly; you can see the current free areas and cut‑offs on the income test for Age Pension page.

While the assets test separately looks at the total value of your assets (including financial assets), deeming itself is an income‑test concept: it converts the value of those assets into a standardised income figure. Your final Age Pension rate is whichever is lower after applying both the income and assets tests, so deemed income can indirectly interact with the asset side by influencing which test becomes the binding one in your case.

Recent Changes to Deeming Rates

Deeming rates were kept at unusually low levels during and after the COVID‑19 pandemic, but the government has since announced a series of increases to bring them closer to achievable market returns. On 20 August 2025, the Minister for Social Services announced that from 20 September 2025 the lower deeming rate would rise to 0.75% and the upper deeming rate to 2.75%, with thresholds of 64,200 AUD for singles and 106,200 AUD for couples combined.

The Department of Social Services notes that from 2026 onwards the Australian Government Actuary will make recommendations on future deeming rates, based on the returns pensioners can reasonably obtain on their investments. Government documents clarify that these changes are intended to more accurately reflect prevailing conditions while still keeping deeming rates below typical returns from common products such as savings accounts and term deposits.

Media outlets have reported that recent and upcoming deeming rate increases can reduce Age Pension and other Centrelink payments for some retirees, effectively acting as a “double whammy” when combined with broader cost‑of‑living pressures. National Seniors Australia and other advocacy groups have emphasised the need for any increases to be gradual and predictable so retirees have time to adjust.

For up‑to‑date policy announcements and official rate schedules, useful links include:

- DSS – Social security deeming rates

- Resetting the Social Security Deeming Rates – impact analysis

- Minister for Social Services media releases

Strategies to Manage the Impact of Deeming

Because deeming applies the same rates regardless of how your financial assets actually perform, you have some flexibility to structure your money to balance Centrelink outcomes with your broader financial goals. However, any strategy should prioritise overall financial security rather than focusing solely on maximising your pension.

Common strategies discussed by financial planners and retirement funds include:

- Review where your cash is held: Since deeming assumes a standard return, you may be able to seek higher interest rates on savings accounts or term deposits without worsening your Centrelink position, provided the total level of financial assets does not change significantly. For broader ideas on diversifying your portfolio beyond cash and deposits, you might find this guide on smart investment strategies for business owners in the USA and Australia useful background.

- Understand how super and account‑based pensions are treated: Once you reach Age Pension age, superannuation balances and income streams become more fully assessable, but the way they are structured can affect both assets and income tests.

- Avoid chasing Centrelink at the expense of returns or liquidity: DSS emphasises that deeming should encourage people to choose investments based on merit, since extra returns above the deeming rate are not counted as income.

- Seek personalised financial advice: Because the interaction between assets, income, tax and Centrelink is complex, financial planning firms often recommend tailored advice rather than do‑it‑yourself restructuring based solely on deeming. Understanding how return on investment is measured across markets can help frame these conversations; this complete guide to understanding ROI in the USA and Australia offers a useful conceptual overview you can apply when comparing options.

Several super funds and advisory firms offer practical guides to managing deeming, such as:

- AMP – What are deeming rates and how 2025 changes could affect you

- Australian Retirement Trust – Deeming rates and Age Pension

How to Check Your Situation and Next Steps

If you are unsure how deeming rates affect your current or future Centrelink payments, there are several practical steps you can take.

- Gather your financial information

List your bank balances, term deposits, managed funds, shares, super accounts and any income streams such as account‑based pensions. Having up‑to‑date figures makes it easier to estimate deemed income. - Use online calculators and estimators

Tools like the SuperGuide Age Pension deeming calculator and the National Seniors Age Pension indexation estimator can give you an approximate idea of how changes to deeming rates might affect your payments. - Review official government information

Check the latest deeming rates, thresholds and policy updates directly from DSS and Services Australia. - Seek personalised advice if needed

If your situation is complex or you are considering restructuring your assets, it is sensible to discuss options with a financial planner or financial counsellor experienced in Centrelink issues. You can also contact Services Australia directly or speak with a community legal centre or welfare rights organisation for free or low‑cost guidance.

By understanding what Centrelink deeming rates are, how they are calculated and how they feed into the income test, you can make more informed decisions about your investments and retirement planning while staying on top of potential changes to your entitlements.